“… ensuring that the ‘power of rules’ prevail over the ‘rules of power’…”

Tanja Fajon, Minister of Foreign Affairs of the Republic of Slovenia,

Bled Strategic Forum, 26-30 August 2022

Introduction

As suggested by Tanja Fajon, ensuring that the power of rules prevails is the main challenge concerning the relationship between the Balkans and the EU. This challenge must be viewed against at least four critical features: the current global geopolitical challenges; the reshuffling from global to regional value-chains; the risks and opportunities deriving from the EU enlargement to the Balkans; and the need for a European structural reform.

1. The global framework

Before the Russian invasion of Ukraine, since at least the US-led financial crisis, the world was in need of (and moving, slowly, towards) multilateralism, as a way to overcome the weakness of a hegemonic system no longer reflected in the real balance of economic and political power worldwide. The conflict put a halt to this process, risking a return to a new form of bilateralism, that very much resembles the doom years of the cold war. The need to provide crucial global public goods for the survival of mankind suggests that we cannot afford such trend.

We must return on the way of multilateralism.

A key responsibility for this is the birth and consolidation of a clear European actorness and sovereignty, in turn depending on the ability of Europe to provide crucial public goods such as ensuring security in the provision of energy, food, raw materials, technology, multi-layered industrial structures, etc. Generally speaking, this requires restructuring the European economy to be more self-reliant; at the same time this implies a single foreign policy and a common strategic attitude towards external partnerships (Africa, Latina America, wider Europe, post-Putin Russia, Mediterranean Basin, etc).

Hence the need to enhance the European cohesion in areas where externalities split over national boundaries, again: security, foreign policy, energy, health, major infrastructure, digital and green transition. This can be done via national coordinated action, which proved weak in times of crisis, i.e when it is most required, and with high risks of asymmetry (due to different financial health of national budgets) or with a joint budget, increased with genuine own resources and/or in deficit spending.

2. Reshoring

One key aspect of this European sovereignty enhancing strategy requires internalizing formerly global value chains. This is an ongoing process since the covid, but should be further pursued.

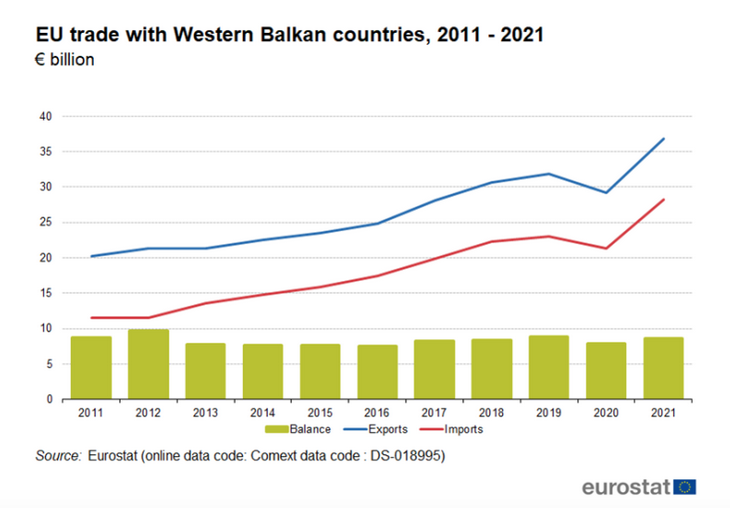

Hence the economic relevance of the Balkans in the EU. The following is a series of graphs and tables illustrating the trade interchange between the Balkan countries and the EU, from both sides.

They testify of a strong interdependence in regional value chains that should be further pursued. Not in an autarchic perspective, that the EU cannot afford anyway, being extremely exposed to external provision of key raw materials, but in a strategy of greater productive autonomy.

The EU current account surplus is constant and comes from an increasing trend of both imports and exports.

Exports are mainly directed to Serbia, which has a leading role in economic terms among the Balkan countries, in particular thanks to the strong engagement of Germany and Italy.

Also from the part of the Balkans, the EU represents over 4/5th of the regional exports and accounts for more than a half of imports. Both China and Russia are currently of minor economic importance to the area. This strategic asset should not be wasted.

3. Critical features

Traditional, historical, geopolitical alliances may be a problem. Serbia’s relations with Russia may be a risk for the strategic unity of the region. But it may be turned into an opportunity. Sooner or later the conflict in Ukraine is destined to come to an end; and we cannot expect simply to ignore the existence of Russia. Some kind of reciprocal relations must be established again between the EU and Russia. In this case, previous privileged relationships with Russia of some member countries may be an opportunity as a political and economic bridge. It is a long-run perspective. But nobody can predict how short this long-run may turn out to be.

Another major risk may be diverging interests between the Balkans. It is not by chance that we use the term Balkanization to illustrate fragmentation. It is in the responsibility of the EU to single out areas where balkanization risks are minimized a strategic unity ensured.

One more risk derives from the current weakness, especially in some of these countries, to ensure the (active) protection of human, civic, social rights and common European values. We do not want more problems similar to those we are experiencing with Hungary and Poland. This will very much depend on the way collective decisions are taken and enforced. We shall return on this later.

One further issue concerning the diverging performance of these countries in economic terms, that will need to be addressed. This also implies a more active redistributive capacity of the EU budget than what it is currently. We shall return on this in the next section.

4. Deepening or enlarging?

I hope I made it clear that the sooner we allow the Balkans in the process of EU membership the better. Pending the implementation of effective powers in foreign policy, the enlargement represented (and still represents) the true, viable EU foreign policy till now, by which the EU extended the power of supranational rules to a growing number of European countries.

Enlarging is therefore unavoidable; to stabilize democratic trends, ensure balanced growth, enhance the resilience of the whole European continent to internal and external challenges. The ADRIA Region is already providing a useful table for common projects in the fields of skills, best practices, human capital, joint investment, etc. It is not enough. Full membership should come as soon as possible.

Deepening, nevertheless, is key too. In particular, no collective decision can be left again to the blackmails of veto power. And this requires treaty changes and an ex-ante agreement, before any enlargement takes place.

A two or three tier Europe might fit for the purpose of accommodating the institutional architecture to the required compromise between enlargement and deepening. Macron’ European political community might serve for this purpose. This implies, nevertheless, that a core of European countries has the strength to increase its collective sovereignty, basically thorough founding a federal system.

Concluding remarks

In any case, what is mostly important is that Europe provides a clear and timely signal of a radical change in its governing structure, showing that it is ready to take the opportunities and minimize the risks of inefficiency, eventually providing a convincing coherence between its decision-making system and the rhythm of history.